Financial Industry Banks on Data, Automation

YOUNGSTOWN, Ohio – Data is king in banking and financial institutions use it to improve efficiency and drive business.

Automation and artificial intelligence allow banks and credit unions to mine mountains of data to identify consumer habits. What is purchased, how it’s paid for – debit card, cash or app – and whether it was purchased in-store or online are tracked to give banks a better perspective.

“That’s the kind of stuff that we’re looking for,” says Melissa Maki, vice president/marketing communications director at The Middlefield Banking Co. “And that uncovers these little gems, these little nuggets of things that we can know to look for in providing our customers with services.”

The idea is to use that information to personalize the banking experience, such as by installing more interactive teller machines or recommending loan products to individuals.

For example, if a customer is using a home equity line for home improvements and the bank notices its customer has little availability but has a low loan-to-value ratio, the bank might recommend a direct installment loan, says Vincent Delie Jr., chairman, president and CEO of FNB Corp. and First National Bank of Pennsylvania.

“We can use artificial intelligence to identify the customers and see what they’re doing – and we can circle back to them and present to them another opportunity,” Delie says. “We use it to help create leads inside the company to drive product sales or product recommendations for changes.”

Banks have been building these data for years as customers shift to online and mobile banking. As the pandemic accelerated that shift, banks strengthened their automation infrastructure to enhance those efforts and roll out new products.

FNB is building a data hub to process large volumes of data from disparate applications under its umbrella. To that end, FNB hired several people with extensive expertise, Delie says.

Similarly, 717 Credit Union is compiling the data it’s accumulated over the years, both digital and on paper, to input into a centralized transaction processing system, says Brian Boettcher, senior vice president for innovation and information technology.

Every transaction will go through the digital core processing system, which should be completed by the end of 2022 or early 2023, he says.

“That’s going to be a big enabler of business intelligence, data management and the digital space because it’ll be a digital system,” Boettcher says.

True artificial intelligence, however, doesn’t exist yet, Boettcher says. What’s currently available is more business intelligence – data gathered and applied to machine learning solutions to improve internal efficiencies.

Customers who call teleservices at 717 initially speak to a machine that learns patterns of speech from hundreds of calls. If a request from a member is for a balance update, the system will identify the member when he calls and give a balance update without being asked, thus improving overall customer engagement.

“Using AI to effectively answer the member’s question without having to go to a human is faster,” Boettcher says. “And it does free up our people to handle the more complex topics so we don’t have people waiting in the queue.”

Doing More with Screens

As more customers turn to mobile options for just about everything, banks and other financial institutions are shifting more products and serv-ices to those platforms.

Upgraded infrastructure will allow for end-to-end digital loan originations and document signing via mobile devices.

FNB recently introduced a mobile eStore, which allows users to conduct routine transactions, purchase products and services, view credit scores and schedule virtual sessions with bankers, Delie says.

In 2022, FNB will introduce interactive eStore kiosks in its branches as part of its Clicks-to-Bricks initiative.

“You have all of your products and services listed on the eStore, and the customer can go in, pick a checking account and loan product, put them in the shopping cart and proceed to checkout,” he says.

FNB saw a 40% increase in mobile banking from the first quarter of 2020 to the same period this year, as well as another 29% increase in online banking, Delie says.

Similarly, Middlefield Bank has seen its consumer-level customers gravitate toward online options for the last few years. From the start of the pandemic, business customers have driven a 76% shift to online or mobile banking tools or both, says Michael Allen, executive vice president and chief banking officer.

Middlefield will soon introduce a consumer-level solution for opening deposit accounts online with another option for small businesses a few months later.

In the first quarter of 2022, the company will add online loan applications and the ability to digitally submit supporting documents, he says.

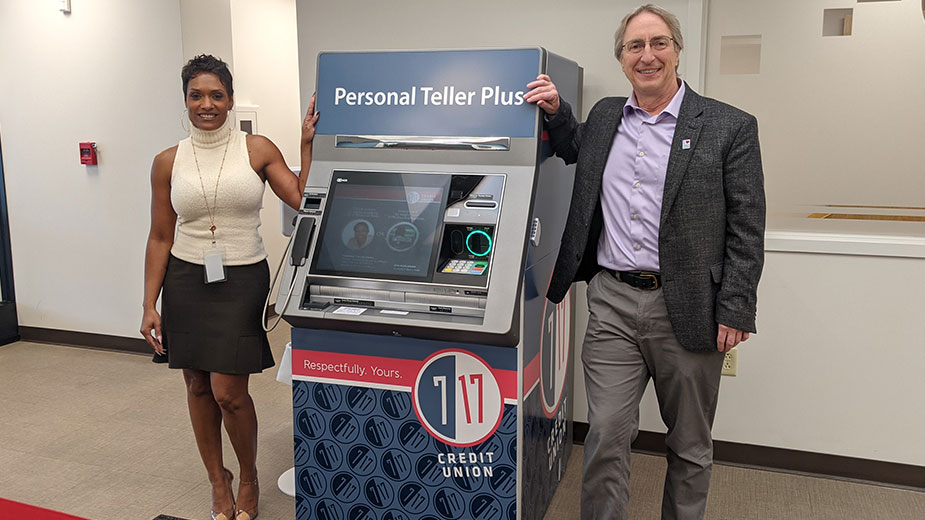

Additionally, financial institutions are implementing more interactive teller machines, or ITMs, which allow users to conduct transactions with tellers via video at a drive-thru rather than enter a branch.

717 has more than 30 such machines in operation in its service area, Boettcher says.

At the same time, traditional ATMs are regaining popularity in the Mahoning Valley; 717 saw its ATM transactions rise 7.9% this year over 2020, he says. “It will be a record year by a significant amount,” he says.

Farmers National Bank has four ITMs at its lab branch on U.S. Route 224 in Boardman and will deploy 10 within the next three months, including those in Canton and at the intersection of 224 and Market Street, says its chief information officer, Brian Jackson.

More Farmers customers are embracing mobile as well, he says, and the company is exploring new solutions including a peer-to-peer payment option, as well as the ability to “turn off” debit cards and track debit activities through a mobile app.

Farmers also looks to expand its mobile solutions among commercial customers, Jackson continues.

“With commercial clients, it definitely gets more complicated because they’re doing more complex transactions,” he says. “You have to be able to make those transactions secure. We go through a huge vetting process and we test these applications thoroughly.”

While the pandemic drove development for mobile solutions, it also brought “an incredible amount of fraud,” Middlefield’s Allen says.

“We needed to bolster the solutions that we had available to us,” he says. “We already had some solutions. But we enhanced those solutions by using what’s called reverse positive pay.”

Many banks adopted reverse positive pay solutions, which mitigate fraud by detecting fraudulent, altered, or counterfeit checks by allowing customers to review prior-day checks that were presented for payment.

“It gives the business owner the control to stop payments in place when they uncover a potentially fraudulent activity,” says Ryan Spisak, PNC business banking market manager.

Banks have also adopted Zelle, a digital payment network, as a way to allow consumers and commercial customers to send money securely online without having to share checking account and bank routing numbers.

Such tools address the increasing need among consumers to send money to friends, while businesses can also use them to pay vendors in real time, Spisak says.

PNC offers several payment and invoicing tools.

“The efficiency is significant because it provides another method for them to electronically transfer funds rather than writing a check,” he says. “It provides them with more control.”

Before 2020, more than 60% of all U.S. corporate payments were done with a physical check, notes Shannon Mortland, vice president of regional media relations for PNC.

But since March 2020, the conversion to real-time, electronic payments “has been astonishing,” she says.

The Future of Bricks-and-Mortar Branches

While there is a shift to mobile, Middlefield’s Allen believes there will always be a need for bricks-and-mortar branches and personal banking.

“The customer wants to see the branch. They want to be able to drive by the branch and know that’s where their money is,” he says. “But their need to interact with the branch will continue to diminish over time.”

This could lead to smaller physical branches, notes Farmers’ Jackson. A branch footprint could likely be reduced to 1,800 to 2,000 square feet and feature more virtual ITMs, much like the Farmers lab branch.

717 recently opened a branch in downtown Warren that’s 1,500 square feet – notably smaller than other branches.

What won’t change, Boettcher says, is the need for people. “We talk about how we can make people better at what they do. And automation, artificial intelligence, business intelligence lets us do that,” he says.

Pictured at top: 717 Credit Union Vice President Remote Delivery Experience Sherri Ramsey and Brian Boettcher, senior vice president of innovation and information technology, with one of the credit union’s ITMs.

Copyright 2024 The Business Journal, Youngstown, Ohio.